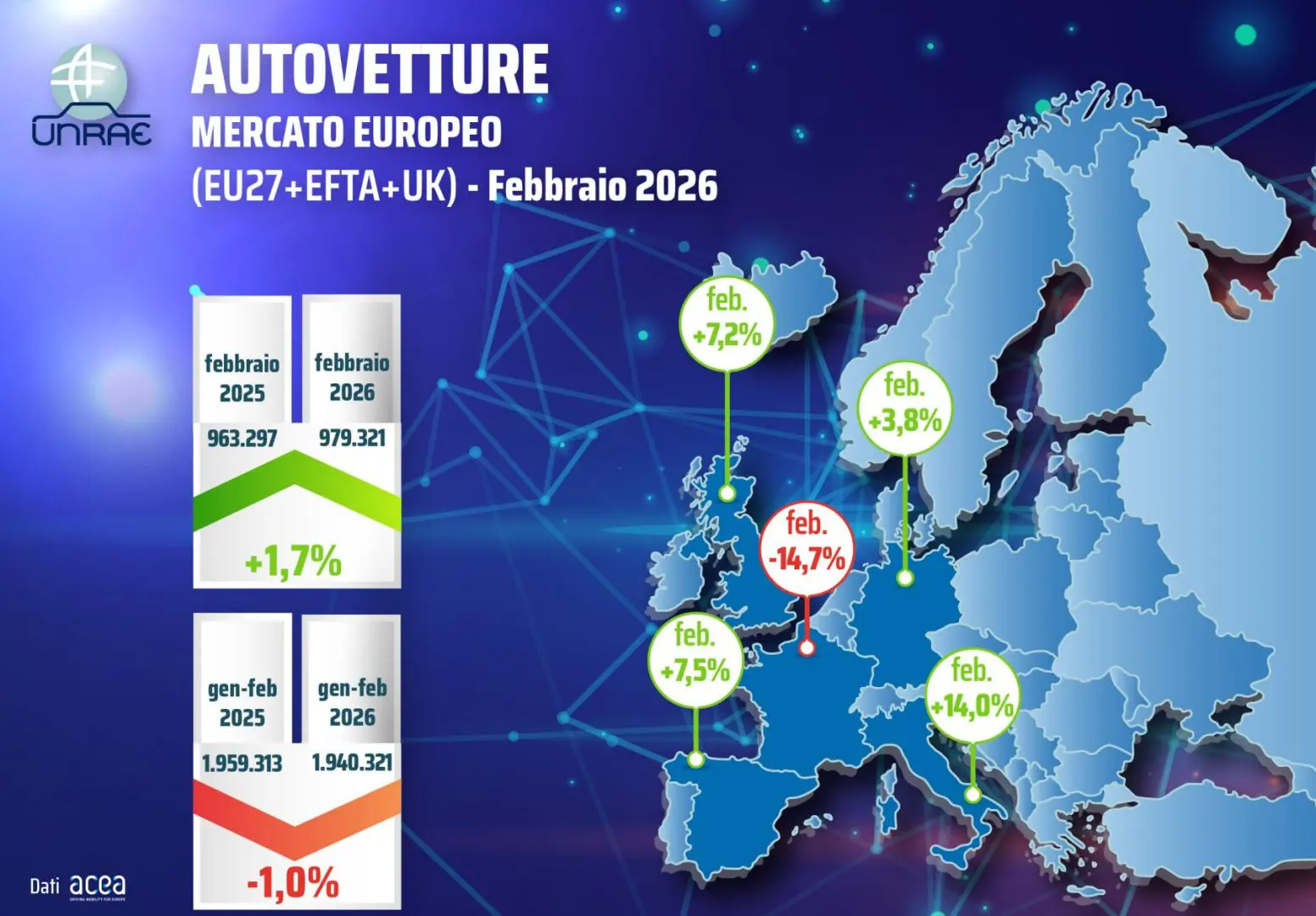

ROMA (ITALPRESS) – The European automobile market returns to a positive result in February, with a modest growth of 1.7%: 979.321 registrations compared to 963.297 of February 2025. In the first two months of the year, therefore, the decrease is reduced to 1.0%, with 1,940,321 units against 1,959,313 in the same period of 2025, but remains a delay of 18.3% compared to the volumes of 2019. Analyzing the trend of the main European markets in the month, a very different picture emerges: France is the only country to record a negative sign, with a decrease of 14.7%, while Germany grows of 3.8%, the United Kingdom of 7.2%, Spain of 7.5% and Italy gets the best performance with an increase of 14.0%.

France yielded 11.1% in the two-month period, Germany 1.4%, while Spain grew by 4.6%, the United Kingdom by 4.8% and Italy by 10.2%. Thanks to these results, Italy gained the second position between European markets both in the month and in the bimonth, as had already happened in January-February 2025. In February Italy is confirmed to last place among the main European markets for share of rechargeable vehicles (ECV), with a total penetration of 16.0%, equally divided between fully electric cars (BEV) at 8.0% – thanks to the MASE incentives that have produced distortionive effects on competition – and plug-in hybrids (PHEV) also to 8.0%.

The difference from other large markets remains considerable: Germany reaches an ECV share of 33.4% (BEV 21.9%, PHEV 11.5%), the United Kingdom of 35.8% (BEV 24,2%, PHEV 11.6%), France of 32.3% (BEV 26.8%, PHEV 5.5%) and Spain of 21.7% (BEV 9.2%, PHEV 12.5%). On the total European market, rechargeable vehicles cover 29.3% of registrations: the BEV stands at 19.5% (+2.4 p.p.) and the PHEV at 9.8% (+2.3 p.p.). Excluding Italy from the count, the BEV share rises to 21,7% and that PHEV to 10.2%. The situation does not change in comparison of the first two-month period: Italy remains a tail light among the main European markets for the diffusion of rechargeable vehicles, with a total ECV share of 15.4% (BEV 7.3%, PHEV 8.1%). The distance from other countries is marked: Germany is at 33.4% (BEV 22.0%, PHEV 11.4%), the United Kingdom at 34.4% (BEV 22.0%, PHEV 12.4%), France at 32.5% (BEV 27.5%, PHEV 5.0%) and Spain at 21.2% (BEV 9.0%, PHEV 12.2%). In the European market, ECVs cover 29.7% of registrations: BEVs reach 19.6% (+2.7 p.p.) and PHEV 10.1% (+2.6 p.p.). Net of the Italian figure, the BEV share rises to 21,8% and that PHEV to 10,5%.

“As UNRAE has not tired of remembering for years, corporate cars represent the main engine of energy transition in the industry. These, in fact, are renewed with a frequency almost triple compared to the private park, feed the market of the used with fresh and modern vehicles at affordable prices and favor the widespread diffusion of technologies with low emissions. Without a tax reform oriented to environmental sustainability – which intervenes on detraibility of VAT, deducibility of costs and duration of depreciation – Italy will not be able to center European goals, correcting the concrete risk of turning into a standard B market,” says Andrea Cardinali, Director General of UNRAE.

Italy continues to record the lowest percentage of company registrations among the main European markets, with a share of 45.8%. The detachment from the other four countries remains structurally significant: in 2025 it was 7.2 percentage points from Spain, 8.5 from France, almost 16 from the UK and almost 21 from Germany, which leads the ranking with 66.4% of business demand.

This comes first of all from a penalizing tax: in most other major European markets the deducibility of costs is integral and the amobile share reaches 100%, while Italy loses a deductible cost still blocked at 18.076 euros (a lire value of 1997) with a shock absorbable price stopping at 20%.

With regard to other factors enabling the energy transition, the country also urgently needs structured interventions to speed up the development of electricity charging infrastructure and ensure a more balanced territorial distribution. In fact, a marked concentration of charging points is observed in the northern areas: the North-West and the North-East collect about 59-60% of the installations altogether, while the South and the Islands stop around 20% of the total. The sizing and localization of the infrastructure should also be planned on the basis of indicators of capillarity – i.e. the number of charging points every 100 km of road – clearly distinguishing between slow and fast reloads, to better meet the specific needs of the different territorial contexts and use. It also seems necessary to encourage the adoption of intelligent charging systems (smart charging) that can optimize the power requirements at the local level, contain the simultaneity of the absorptions and enhance the potential of the vehicle-to-grid (V2G). At the same time, it is essential to plan adequate investments for the modernization and strengthening of electrical networks and medium voltage cabins, especially in urban areas, where the highest demand for charging is concentrated.

“On the side of the question, Italy is in a position of net disadvantage: in our country there is currently no incentive plan for the purchase of BEV and PHEV cars, while all the other four major European markets have active support programmes. In particular, all measures in force include private individuals, in the United Kingdom and Spain are also extended to legal persons. France and Spain are limited to 2026, while the United Kingdom and Germany are distinguished by multiannual plans that guarantee stable planning over time,” concludes Andrea Cardinali.

– photo Unrae –

(ITALPRESS).