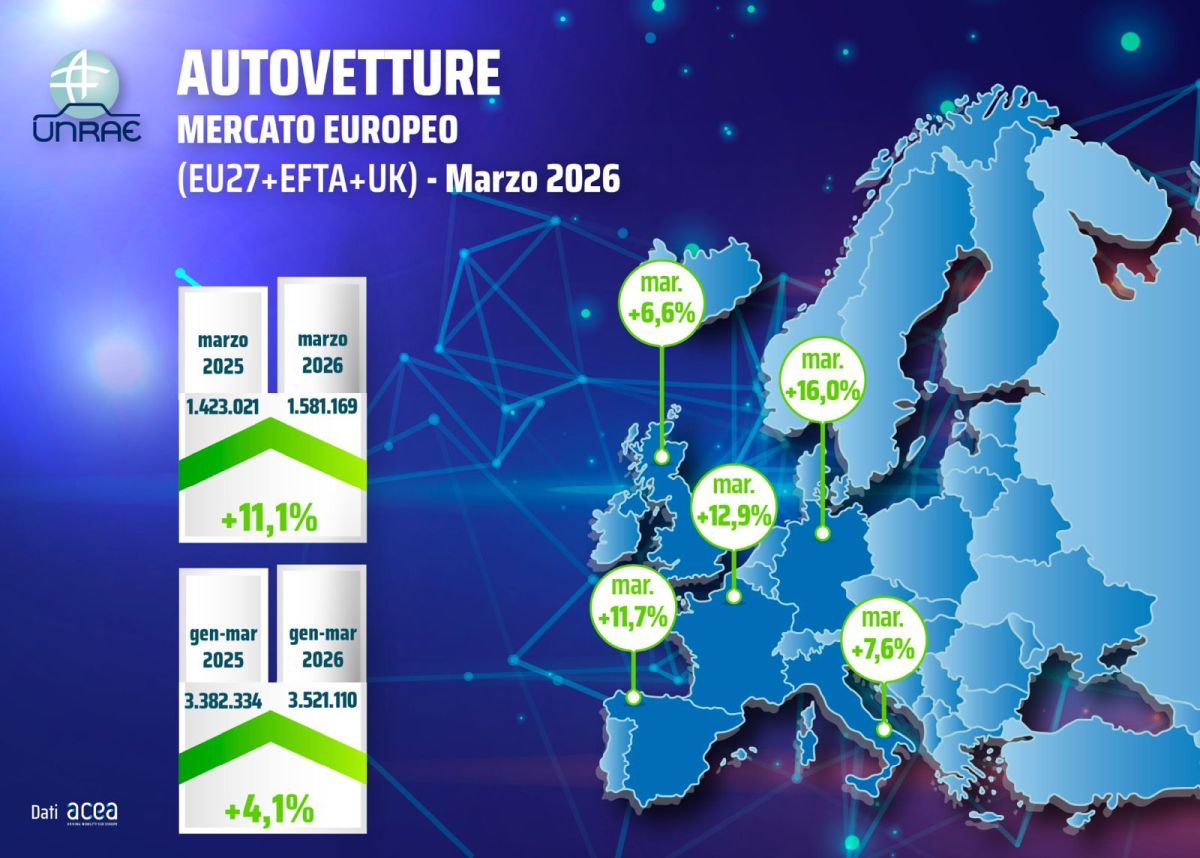

ROMA (ITALPRESS) – The European motor vehicle market stores March 2026 with a strong and widespread growth between countries (28 on 31), attesting to 1,581.169 registrations, up 11.1% compared to 1.423.021 units of the same month of 2025. A result that consolidates the positive trend already emerged in the previous months and that brings the budget of the first trimester to 3.521.110 registrations, with an increment of 4.1% on the 3.382.334 of the correspondent period last year, while still remaining below 15.1% regarding the levels of 2019. In March all major European markets have a positive sign. Germany leads the ranks with a jump of 16.0%, followed by France to +12,9% and from Spain to +11.7%. Italy stands at +7.6%, while the United Kingdom scores a +6.6%, totaling the best volume result for the month of March from 2019, thanks to the half-year change. Italy occupies the third position in the Major Market ranking as in March 2025 and as in the first quarter of this year. On the front of the rechargeable cars, the month of March confirms Italy in the last position among the major markets of the Union for share of rechargeable cars (ECV), with a total penetration of 17.2%, of which 8.7% reported to electric battery cars (BEV) – with a third of the total concentrated on a single brand – and 8.5% to plug-in hybrids (PHEV). The difference from other markets remains considerable: Germany reaches an ECV share of 34.2% (BEV 24,0%, PHEV 10.2%), the United Kingdom of 35.6% (BEV 22.6%, PHEV 13,0%), France of 33.2% (BEV 28.5%, PHEV 4.7%) and Spain of 20.5% (BEV 9.1%, PHEV 11.4%). At the aggregate European level, the rechargeable cars represent 31.8%, with the BEV at 21.8% (+4.7 points compared to the previous year) and the PHEV at 10.0% (+1.6 p.p.); excluding the Italian data, the BEV share rises at 23.5%. The analysis of the first quarter of 2026 returns a similar picture: Italy is again ranked in the last place among the main markets for the diffusion of rechargeable vehicles, with a total incidence of 16.2% (BEV 7.9%, PHEV 8.3%). Comparison with European partners highlights significant distances: Germany with ECV at 33.7% (BEV 22.8%, PHEV 10.9%), United Kingdom at 35.2% (BEV 22.4%, PHEV 12.8%), France at 32.8% (BEV 27.9%, PHEV 4.9%) and Spain at 21.0% (BEV 9,1%, PHEV 11.9%). As a whole of the European market, the ECV reached 30.7% of the share, with the BEV to 20.6% (+3.6 p.p.) and the PHEV to 10.1% (+2.2 p.p.); net of Italy, the BEV share rises to 22.6%. In line with the European emissions reduction targets, UNRAE reiterates the urgency of a reform of corporate car taxation in green key, aimed at speeding up vehicle penetration at zero or very low emissions – up to 60 g/km CO2 – in the national market. It is essential to act on detraibility of VAT, deductibility of costs and period of depreciation, through progressive measures that take priority start from the revision of the deductibility scheme. Such interventions would also reduce the competitive gap between Italian companies of any commodity sector and their European counterparts. Director General Andrea Cardinali stresses that: “According to the latest ACEA report on tax benefits and incentives for electric cars, published in mid-April, tax concessions for electric traction business vehicles are a powerful tool to speed up fleet electrification, so that 18 EU Member States have adopted them, in different ways. Among the main markets, Germany intervenes with accelerated amortisation that, together with 100% VAT deductibility in line with Community discipline, translates into a cost for the company less than 40% compared to Italy. United Kingdom applies aliquote fispreferential calibrations for BEV, Spain accelerated amortisation. In this context, the total absence of measures dedicated to business cars in Italy, unique among the five European Major Markets not to have them.” Cardinals point out that political intervention is no longer necessary: “The adoption of the proposals that UNRAE has long submitted to the Institutions would be a decisive step to combine the achievement of environmental objectives with the strengthening of the competitiveness of the productive system, while at the same time supporting technological innovation and the renewal of the circulating park.” Renewal of the park is an absolute priority in environmental and road safety. With more than 41 million cars in circulation at 31 December 2025 (UNRAE estimate), the Italian park is one of the most extensive in Europe in relation to the population and, at the same time, among the most dated and polluting in the main markets of the Continent: with an average age of 13, our country is second only to Spain for seniority, but with dimensions greater than once and a half. The progressive anagraphic and technological ageing of the fleet therefore appears unreliable, considering the active and passive safety features and the technologies of reduction of emissions obligatoryly present in new generation vehicles. In parallel, for the development of the energy transition, Italy urgently needs an accelerated plan of infrastructure of electric charging, with a territorially homogeneous distribution, and interventions on charging costs, so that the tariffs are in line with those practiced abroad.

photo: UNRAE press office

(ITALPRESS).